What is the impact of the US Federal Reserve’s decision to increase interest rates? As you are likely aware, on Wednesday December 16th 2015, the US Federal Reserve announced their decision on monetary policy for the coming months including an increase in interest rates of 25 basis points (0.25%). While this increase is yet another signal of a healthy US economy (a great sign for the value and demand for our rental properties), this also marks the first interest rate increase since the Fed dropped the rate to near zero in 2008.

Many are likely wondering about its impact on their investments in the United States, specifically in the Phoenix market. The following is intended to help provide you with our insights on the subject.

By The Numbers

For every 0.25% increase in the variable interest rate and $1,000,000 in loan amount, the interest payment will increase $2,500 per year or $208.33 per month. To put this in perspective, our average asset in Phoenix has an $8 million loan and consists of 200 units. For this example, the mortgage payment would increase $20,000 per year or $1,667 per month.

This equates to an increase of approximately $8.33 per unit, per month in mortgage payments. In the past year we have increased monthly rents an average of $87.00 per unit (not including washer/dryer revenues) and we continue to see the strong indicators for future growth.

In November we returned to investors cash flows averaging 8.8% of invested capital. The 0.25% interest rate increase, without any mitigation, would have reduced the returns to approximately 8.3%.

Why The Increase?

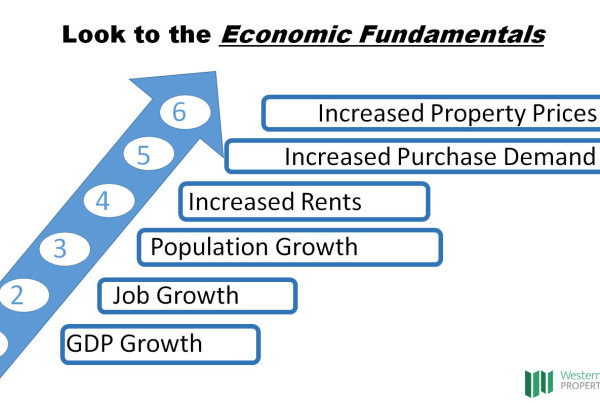

Here’s the good news: the Fed is increasing interest rates because the economy is growing in the United States, especially in Phoenix which is forecasted to be the second strongest job growth market in the United States in 2016. With the national unemployment rate down around 5%, considered full employment, the Fed is expecting wage growth which should increase inflation. Wage growth and inflation are very positive for real estate investments.

We have chosen the path of variable rate mortgages because of the deep discount in interest rate (1.5% – 2.0% discount) and as we believe that although we have seen a single rate increase we will not continue to see significant increases in the near-term that would warrant the additional costs of fixed-rate mortgages.

In conclusion, when we see rates go up, there can be some media bias that will lead some to believe that this is a bad thing, but ultimately the move is a vote of confidence. There is job growth in the region, which leads to inflation and that means rents are rising and property values are increasing. As long as the rent increases exceed the increase in the cost of financing, this is good news for all investors.